People in the business community right now are quite puzzled as to how they would remit Government taxes as withholding agents. Just last year, December 19, 2017, the new Tax Reform for Acceleration and Inclusion (TRAIN) also referred to as Republic Act (RA) No. 10963, was signed into law by President Rodrigo Duterte.

Inclusive in this tax reform is the change pertaining to tax filing (amended Section 58 of the NIRC). Before TRAIN, the filing of withholding tax was done monthly. Now, the law states that it should be done on a quarterly basis.

This implies that expanded and final withholding taxes should be filed and paid not later than the last day of the month (of the current quarter) during which ‘’tax withholding’’ was made. For example, for the first quarter of the year whose end is on March 30, the taxes shall be remitted on or before April 30.

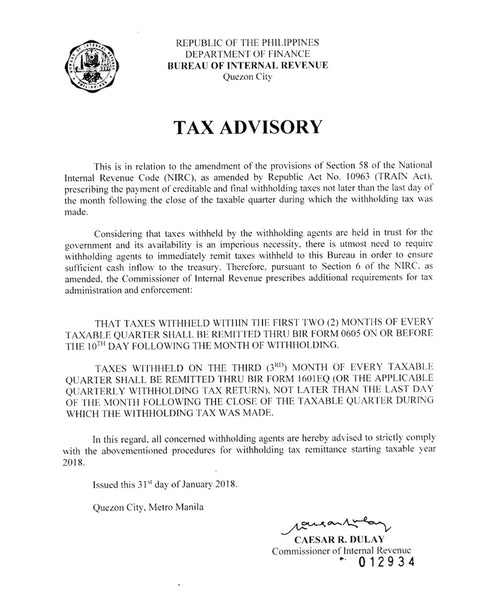

Everything was clear on the side of the taxpayers. However, the BIR made an appeal last January 31, 2018. Considering that taxes withheld by the withholding agents are held in trust for the government and its availability is an imperious necessity, BIR emphasized that there is an utmost need to require withholding agents to immediately remit taxes withheld to this Bureau in order to ensure sufficient cash inflow to the treasury. Thus, the confusion started.

To address such conundrum, the Bureau of Internal Revenue released a Tax Advisory on January 31, 2018 pertaining to the remittance of withholding taxes.

The Commissioner ordered that the taxes withheld for the first two (2) months of the quarter shall be paid using BIR Form 0605 on or before the 10th day following the month of withholding and on the end of the quarter BIR Form 1601EQ (a new BIR form but not yet available for use) will be used and will be filed and paid on the last day of the month following the close of the quarter which the withholding was made.

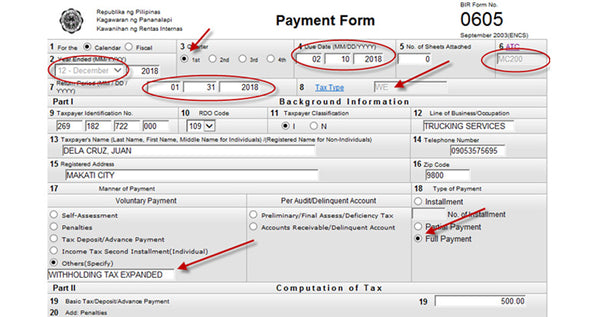

However, the BIR advisory has not specified how the taxpayer will go about using the BIR Form 0605 which is only known to practitioners and businessmen as the Form used to pay delinquency taxes, penalties and surcharges.

The questions such as what Alpanemeric Tax Code (ATC) to use, tax type, due date and period covered are still unknown.

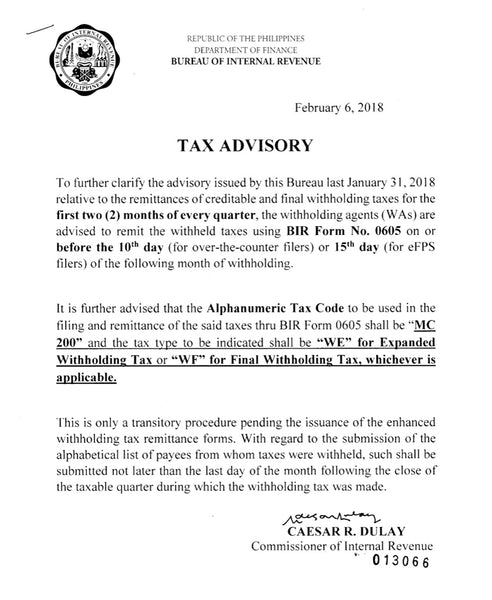

Luckily on February 6, 2018, an advisory from the Bureau was issued to finally address the issue.

The advisory states that in filling up you 0605 for withholding taxes, MC 200 or the Other Miscellaneous Taxes will be used and WE (Expanded Withholding) or WF (Final Withholding tax) as tax type.

Please see image below to be guided when filling out the BIR Form No. 0605 when remitting Expanded and Final Withholding Tax.

For more information, please refer to www.bir.gov.ph.